Trading system failure is defined as the breakdown of a strategy’s ability to produce consistent results when moved from design to live execution. Most traders focus on finding the perfect setup, but the real problem is almost always somewhere else. To identify why trading systems fail, you need to look at execution quality, market regime shifts, emotional interference, and flawed backtesting. These four forces account for the vast majority of blown accounts and abandoned strategies. Tradergibkey has spent over 18 years watching traders repeat the same mistakes, and the patterns are clear.

Why do trading systems fail in live execution?

Execution failure is the most underestimated cause of system breakdown. Retail traders spend about 90% of their effort on strategy design but only 10% on execution quality. That imbalance is exactly why a system that looks great on paper collapses the moment real money is involved.

The gap between a backtest and a live trade is wider than most traders realize. Slippage, spreads, and partial fills all eat into your edge before you even close a position. Transaction costs like slippage and spreads can create hidden annual performance drag exceeding 10%, while overtrading alone reduces annual returns by 3%–7%. That means a strategy with a 52% win rate can turn negative purely from costs.

Technical issues compound the problem. Production failures often stem from overlooked issues like timezone shifts causing missed orders or stale data feeds, not purely strategy flaws. These are the kinds of problems that never show up in a backtest.

Common execution pitfalls include:

- Slippage on fast markets: Your entry fills at a worse price than expected, shrinking your reward-to-risk ratio.

- Partial fills: You size a trade for 10 lots but only get 6, making position management inconsistent.

- Timing mismatches: Signals fire at the close of a candle, but your order executes at the open of the next, creating a different trade entirely.

- Broker API errors: Latency or connectivity drops cause missed entries or duplicate orders.

Pro Tip: Run a monthly execution audit. Compare your intended entry prices to your actual fill prices. If the gap is consistent, you have a structural cost problem, not a strategy problem.

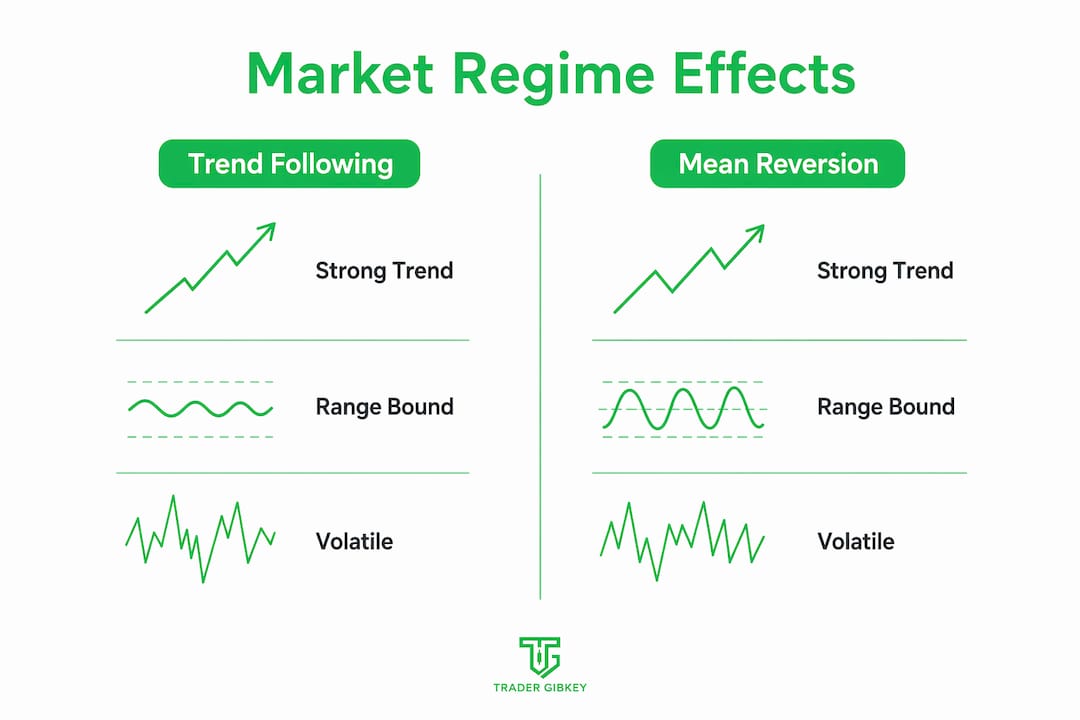

How do market regime changes cause strategy failure?

A strategy built for one market condition will fail in another. Changing market regimes such as trending, ranging, and volatility shifts substantially affect strategy effectiveness. A trend-following system that thrives in a strong directional move will bleed out in a choppy, sideways market.

Most traders build and test their systems during a specific period in market history. That period has a character. It might be low volatility and trending, or high volatility and mean-reverting. The strategy learns that character. When the character changes, the strategy has no answer.

The table below shows how different market regimes affect common strategy types:

| Market regime | Trend-following systems | Mean-reversion systems |

|---|---|---|

| Strong trend | Performs well | Struggles, fights the move |

| Sideways/ranging | Loses on false breakouts | Performs well |

| High volatility spike | Unpredictable, wide stops hit | Dangerous, gaps invalidate levels |

| Low volatility compression | Minimal signals, small gains | Works but with tight ranges |

Regime awareness is a skill, not a feature you add to a strategy. You need to know what conditions your system was designed for and stop trading it when those conditions are absent. This is one of the most common trading system pitfalls, and it is almost never discussed in basic trading education.

Overfitting makes this worse. When you curve-fit a strategy to a specific historical period, you are not building a system. You are building a memory. That memory has no value in a new market environment.

What emotional and behavioral patterns break trading systems?

A valid strategy can fail entirely because of how you execute it. Inconsistent application of strategy rules driven by emotions, such as skipping signals, varying position sizing, and revenge trading, are among the most common reasons systems fail. The strategy logic stays sound. The execution does not.

Here is how the breakdown typically unfolds:

- You skip a signal. The setup looks right, but you are nervous after two losing trades. You sit it out. The trade wins. Now you are frustrated and second-guessing your rules.

- You size up to recover. After a loss, you increase your position size to “make it back faster.” This is revenge trading. It changes your risk profile and often leads to a larger loss.

- You exit early. A trade moves in your favor, but you close it before the target because you are afraid of giving back profits. Your actual reward-to-risk ratio drops below what your backtest assumed.

- You add filters on the fly. You start adding conditions that were never in your original rules. The strategy you are trading no longer matches the one you tested.

Traders fall into what Tradergibkey calls the “strategy trap,” where emotional variance during execution skews results away from backtest expectations. The brain stops trading the chart and starts trading the pain.

Pro Tip: Write your rules down before the trading session starts. Treat every deviation as a data point. If you deviate three times in a week, that is a process problem, not a market problem.

Building a consistent trading process is the single most effective defense against emotional interference. Without it, even a statistically sound strategy will underperform.

What strategy design flaws cause systems to break down?

Poor construction is a silent killer. Overfitting causes roughly 45% of trading strategy failures by making the strategy too narrowly tuned to past data. The backtest looks perfect because the system has memorized noise, not signal.

Poorly defined or overcomplicated strategies with unclear rules lead to inconsistent execution and failure. Adding too many parameters or filters creates conflict and analysis paralysis. The system becomes fragile. One market shift and it falls apart.

Unrealistic backtesting assumptions are equally damaging. Most retail backtests ignore slippage, assume perfect fills, and exclude transaction costs. The result is a performance curve that looks nothing like what you will experience live. Survivorship bias in historical data compounds this, because you are testing against assets that survived, not the full universe that existed at the time.

The fix is to test for robustness, not perfection. A strategy that works across multiple instruments, timeframes, and market conditions is more likely to survive than one that was tuned to a single chart. You can read more about avoiding overcomplicated systems to understand where most traders go wrong in the design phase.

How to fix trading failures and build a more reliable system

Diagnosing and fixing system failures requires a structured review process. Here is where to start:

- Track execution quality monthly. Compare intended fills to actual fills. Measure slippage per trade and total transaction costs as a percentage of gross profit.

- Define your market regime filter. Before trading each week, identify whether the market is trending, ranging, or in a volatility spike. Only deploy strategies suited to that regime.

- Audit your rule adherence. Keep a trade journal that records not just outcomes but whether you followed your rules. A win from a rule deviation is still a failure of process.

- Apply hard risk limits. Professional traders limit risk to 2%–5% per trade. Large losing trades erase gains rapidly. Hard limits prevent one bad session from destroying a month of work.

- Run a quarterly strategy review. Check whether your system’s performance metrics are degrading over time. Tracking alpha decay, the gradual erosion of edge due to market saturation or changing conditions, helps you catch a dying trading system before it wipes your account.

- Validate in live markets before scaling. Paper trading and backtesting are starting points. Validating your Forex strategy in real market conditions with small size is the only way to confirm your edge is real.

The goal is not to build a perfect system. The goal is to build a system you can execute consistently and review honestly.

Key Takeaways

Trading systems fail because of execution gaps, regime mismatches, emotional interference, and flawed design. Fixing these requires process discipline, honest review, and a willingness to adapt.

| Point | Details |

|---|---|

| Execution costs destroy edge | Slippage and spreads can drag annual performance by more than 10%, turning a winning strategy negative. |

| Regime awareness is non-negotiable | A system built for trending markets will fail in ranging conditions. Know your regime before you trade. |

| Emotional deviations compound losses | Skipping signals, revenge trading, and inconsistent sizing all degrade system expectancy over time. |

| Overfitting creates false confidence | Strategies tuned too tightly to past data memorize noise and collapse when conditions shift. |

| Process discipline is the real edge | Consistent rule adherence, monthly audits, and hard risk limits protect performance more than any indicator. |

What 18 years of watching traders fail taught me

Most traders I have worked with over the years did not fail because their strategy was wrong. They failed because they never built the infrastructure to support it. The strategy was the easy part. The hard part was execution, consistency, and the willingness to look honestly at what was actually happening.

The traders who improve fastest are the ones who stop asking “why did the market do that?” and start asking “why did I do that?” That shift in focus changes everything. You stop chasing better setups and start building better habits.

One thing I see constantly is traders abandoning a system after a drawdown that falls well within its historical parameters. They do not know their system well enough to recognize normal variance from actual failure. That is a design and education problem. If you do not know what your system is supposed to do in a losing streak, you will always quit too early.

The other pattern I see is over-engineering. Traders add indicator after indicator, filter after filter, trying to eliminate all losing trades. That is not how markets work. Every filter you add also removes winning trades. The goal is a system with a real edge that you can execute without hesitation, not a system that looks perfect on a chart.

For real, the traders who last are not the ones with the best strategies. They are the ones who built a process, stuck to it, and reviewed it honestly. That is the whole game.

— Gabriel

Tradergibkey resources for stronger trading systems

If you recognized your own patterns in this article, you are already ahead of most traders. The next step is building the structure to do something about it.

Tradergibkey offers practical, experience-based resources covering risk management, strategy validation, and performance review. With over 18 years of live market experience behind every lesson, the focus is always on what actually works, not what looks good in a backtest. Whether you are dealing with execution problems, emotional interference, or a strategy that stopped performing, the Tradergibkey trading resources give you a structured path forward. You will find guides on avoiding retail trading traps and building systems that hold up when real money is on the line.

FAQ

Why do most trading strategies fail in live markets?

Most strategies fail because execution costs, slippage, and emotional deviations erode the narrow edge the strategy was built on. A strategy with a 52% win rate can turn negative from transaction costs alone.

What is the most common trading system mistake?

Overfitting to historical data is the most common design mistake, causing roughly 45% of strategy failures. The system memorizes past conditions instead of capturing a repeatable market edge.

How do I know if my trading system is failing or just in a drawdown?

Track whether your rule adherence and execution quality remain consistent during the losing period. If you are following your rules and the drawdown stays within historical parameters, it is likely normal variance, not system failure.